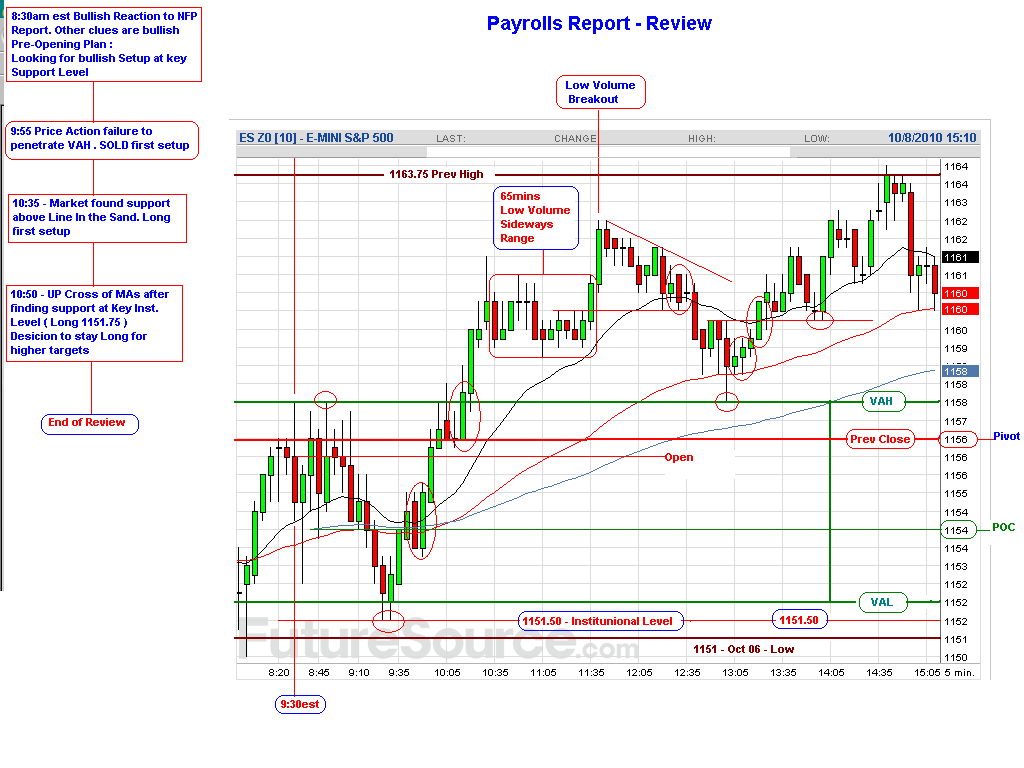

Breakout Trade :

Long 1157.50

Setup : Daily NR45 , Bullish reaction to BOE rate decision during Globex

First Target filled at 1060.50 for + 3 pts profit per contract. Second Target never reached. Out FLAT

at 1060 for another + 2.5 pts.

Total GAIN : + 5.5 Pts per contract

For the short-term, I see a good potential for further consolidation with some emerging downside pressure.

Today brought something for everyone: the Dow advanced, the S&P 500 held steady, but the Nasdaq 100 declined. The Dow is now at its highest closing level since early May of this year.

Today's volume output on the S&P 500 was comparatively elevated, though lower than yesterday's strong volume - 3.42 billion shares were traded. There was a lack of demand, as can be determined by the decrease in volume activity, but in the absence of demand, sellers did not step in to take advantage of the buying void and push price lower.

The Fed keeps feeding money into the corrupt banking system ( Permanent Open Market Operations ), and the banks buy options to support the market. After all, elections are coming up, and the corporate federal government will do all it can to save face for Republicans against the embarrassment of a declining stock market.

The market traded mixed today with only the Dow making further upside progress. One reason for the flat overall performance was seen in lackluster economic data pertaining to the US labor market (discussed below). Intraday, the Dow extended its run to a five-month high, but higher levels were rejected on the S&P 500 as well as on the Nasdaq 100 (which thus showed non-confirmation).

Today saw the release of the ADP payrolls report which typically precedes the government's official 'jobs report' by a few days. Based on the ADP report, some market commentators estimate that this Friday's jobs report could show a modest growth in new jobs. ADP data pertains to private jobs and today's data shows that private employers cut 39,000 jobs in September (consensus estimate: a growth of 18,000 jobs), the first loss in seven months. Today's downside surprise acted as a damper on investor enthusiasm in spite of the fact that data for the prior month was revised upward, suggesting an extra 10,000 payrolls. Market observers suggest a poor jobs report on Friday might further increase the odds the Fed will have to step up its efforts in trying to stimulate the US economy.

In earnings reports (the Q3 earnings season will officially start tomorrow with Alcoa's release), Monsanto fell short of expectations and issued downside guidance.

In the Treasuries market, yields on notes with maturities of 2-, 3-, 5-, as well as 7 years all set record lows today. Treasury yields have been making new lows as investors anticipate there could be further easing (i.e., bond purchases) from the Fed. The US dollar suffered yet another loss against a basket of currencies, losing another 0.5% today and making an eight-month low. Gold meanwhile ran to yet another new all-time high.

In M&A news, Dow component Johnson & Johnson will buy Dutch biotechnology company Crucell NV for roughly $2.4 billion.