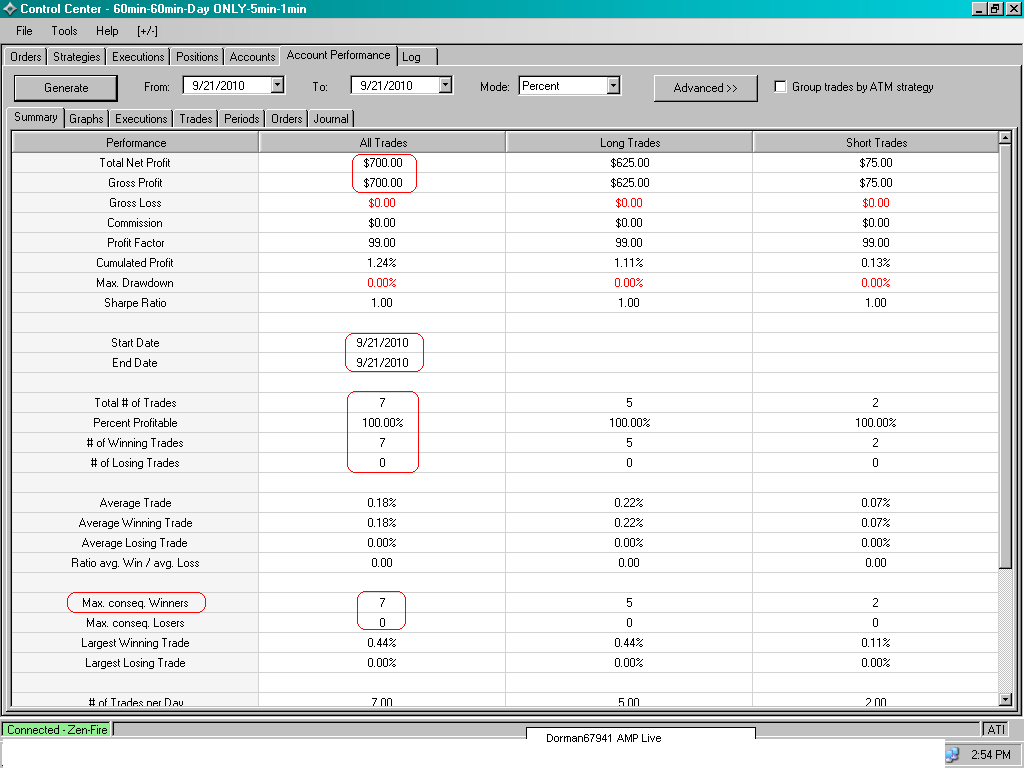

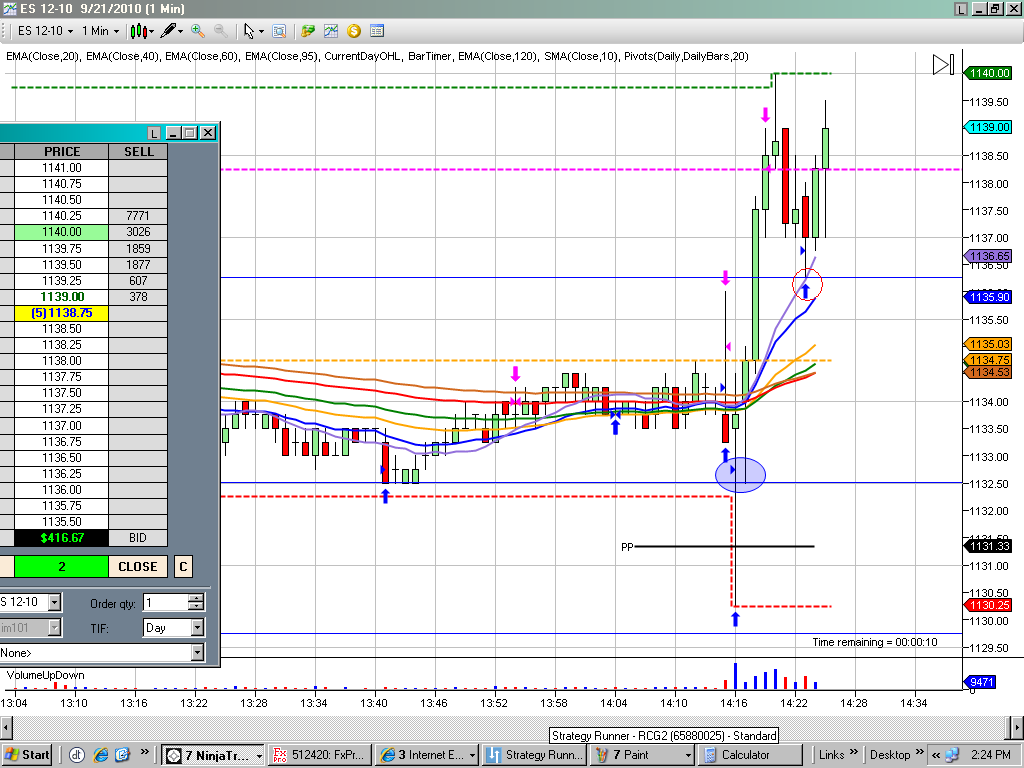

Long from 1054.25 , August 31st :

Open profits : + 73.25 Points

$ 3,662.50 per contract

Friday, Sept 17

" It's About Jobs Stupid "

Watching CNBC this morning, just heard this phrase from a Guest named Bernie Marcus.

This guest either suffers from Selective Amnesia ,

amnesia about particular events that is very convenient for the person who cannot remember, or he is just a pathological liar, either way it is a self serving attitude.

My responce to this guy : It is the Jobs Stupid . The undisputed historical facts are that it was the trade policies of the republican administrations that gave away millions of jobs to the Chinese Communists.

It is the Jobs STUPID : It is the jobs that were NOT created during the Bush Administration.

the fact is that the Bush years -- which were full of across-the-board tax cuts -- turned out to be the weakest eight-year span for the U.S. economy in decades.

It is Jobs STUPID : It is the lack of jobs that the American soldiers returning home will not have if the Republicans take over Congress, STUPID !

Republicans — and some Democrats — want to make all the tax cuts permanent or at least to extend them as long as the economy remains fragile. They fear that a tax increase would hurt the economic recovery.

Well, we all know that neither of those is going to happen. Republicans won't abandon their wealthiest donors to help out everyone else. The GOP will continue to block extension of tax cuts for the middle class unless the rich get theirs too.

So either all the Bush tax cuts will expire unless the Democrats cave and extend all of them. Of course extending tax cuts on the wealthiest Americans (those with incomes in excess of $200,000 for individuals or $250,000 for families) will only increase future deficits more, but that won't stop Republicans from claiming the deficit is all the fault of Democrats and "entitlement programs" (you know, Social Security and Medicare which are subject to a separate, regressive tax).

As for spending, thanks in large part to the costs of our wars in Afghanistan and Iraq, deficits will remain high (and no, our involvement in Iraq isn't over when you still have 50,000 US troops there). The companies that make bullets, bombs and drones and electrocute soldier in showers (Hi KBR!) will continue to do well, but everyone else will suffer from lack of spending.

Without some easing of credit for small business or government investment in rebuilding and modernizing our infrastructure (updating the electrical grid so that it loses less electricity, spending on or tax credits for new green technologies like wind and solar, fixing bridges and roads, investing in education, transportation, etc.) new jobs will be hard to come by.

The Democratic campaigns for the Fall should be be emphasizing that we are falling behind other developed nations because we refuse to INVEST in the infrastructure and new technologies that will secure more jobs now and better paying jobs in the future.

However, it seems the Dems are falling into the GOP trap of having the debate over the Bush tax cuts for the rich and corporate welfare that allows jobs to be outsourced overseas which we know failed to generate job growth in the past

Three million piddling jobs created in 8 years during the Bush Administration? ( Wall Street Journal article )

Remember, this came during a time when Bush increased government spending to private companies and to pay for our massive wars in the Middle East. It was the worst job creation during an economic recovery (from the recession created after the Tech stock bubble burst in 2000) ever. So why on God's Green Earth would any Democrat talk about tax cuts as being the panacea to our nation's job woes?

Every time a Republican says tax cuts create jobs a Democrat should be waving that Wall Street Journal article in his or her face. Every time they say we need to extend the Bush tax cuts for the wealthiest Americans we should be saying that isn't going to create jobs for the unemployed because the record proves it. Bush's job creation didn't even keep up with the rise in the workforce population.

In addition, during the halcycon years of the Bush tax cuts, 8.3 MILLION more people fell below the poverty line during his eight years. Median incomes fell from $52,500 at the end of 2000 (Clinton's last year)to an inflation adjusted $50,303 in 2008 That's a drop of 4.2 per cent.

So who benefited from the tax cuts? Not people who needed jobs, not most workers, not poor people. No, the people who most benefited from the tax cuts were MILLIONAIRES and BILLIONAIRES

So why are Democrats still talking about tax cuts? Eight years of tax cuts and Republican mismanagement cost us jobs, made health care more expensive or unavailable for more Americans, substantially increased poverty and lowered incomes for most Americans. That's the message Democrats should be speaking out about loudly and clearly at every campaign stop and in every speech and in every ad they run this year.