Everyone is waiting for the breakout of the Daily sideways range, now 23 days old.

Is it going to be higher or lower?

Historically, holidays are often accompanied by trend changes in the equity markets. The most noticeable of these is the year end holidays.

Trends that remain in place past November's Thanksgiving holiday usually continue until the beginning of the new year. Then in the first or second week of January the trend ends. This phenomenon was clearly observable in 2008 and 2009, and in four of the past five years

Fridays's action was split, with the NASDAQ 100 rallying immediately after a strong gap up opening, but with the Dow and the S&P 500 initially sliding below yesterday's lows and then bouncing to modestly green closes. All in all, the major indexes continue their range-bound trading, with the NASDAQ 100 currently closer to its 2009 highs than the S&P 500 and the Dow. In fact, the Dow - long the leading index - is now underperforming.

The internals are no longer confirming the market. Banking and housing are but a couple of examples of relative weakness, which also serve as warnings. Yet, the mainstream media and politicians have the masses lulled to sleep. In my opinion this is a great disservice as it only helps to set the stage for the slaughter that will ultimately follow once the Phase II decline begins. In the meantime, the longer this bear market rally lasts, the more damaging it will ultimately be once it is over.

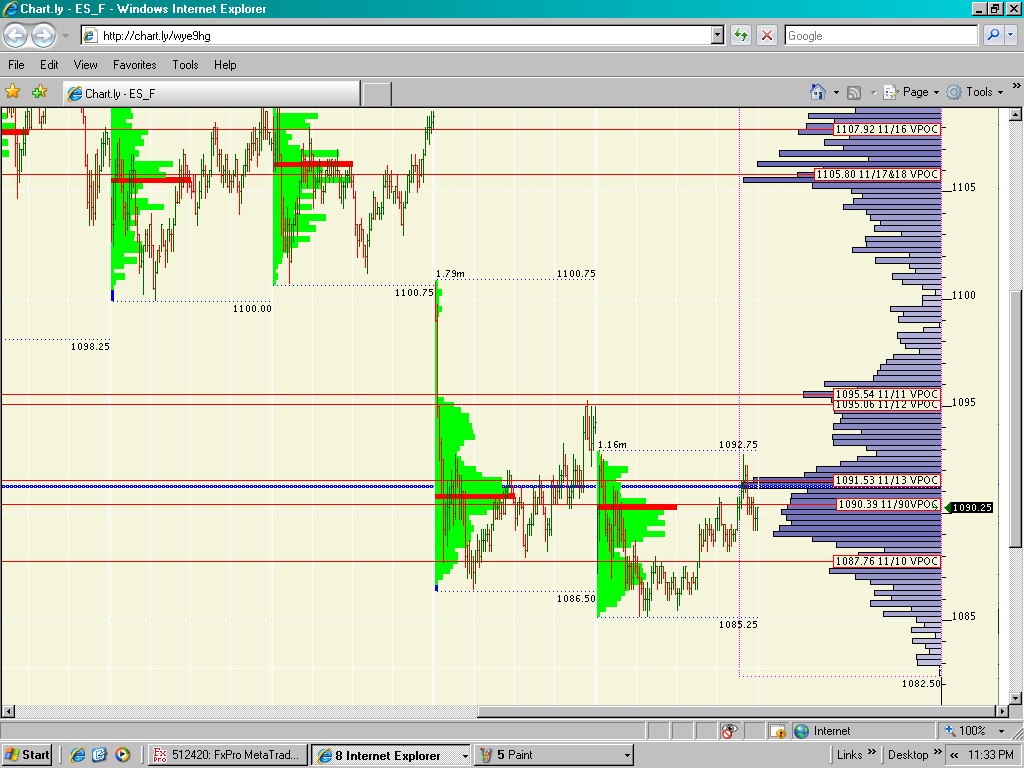

The E-Mini S&P500 ( ES ) closed the week one tick above the 20 Day Moving Average. The US Dollar Index close the week above the Daily Green MA and above the key resistance 77.50, first time since April . There is a high probability that the ES will gap higher before it opens on Monday.

Notable about Friday's session was the relative absence of the sharp volatility often seen during quadruple witching days, but then again, the market has been characterized by low volatility and range-bound, uneventful trading for at least a month. Volume was very high however, largely due to issues being added / dropped from the S&P 500 index. Volume production on the S&P 500 was 47% above the index's average daily volume generation seen over the past three months. 5,644 million shares changed hands on the index traded today.

Technology issues were clearly in the lead today - notice the difference in the trading patterns between the Nasdaq 100 (very strong gap up opening and an uncorrected surge to the top of its recent range near 2009 highs) and the Dow and the S&P 500 (an early dip below yesterday's lows with a subsequent intraday recovery, but much weaker closes clearly off the 2009 highs). Market observers explain the pattern with two large-cap technology issues boosting investor confidence for a recovering economy: Both Oracle and Research in Motion (as discussed yesterday) reported earnings that beat expectations. Oracle provides software for large businesses, and its positive earnings make the case that such companies are becoming more willing to spend on technology. While consumer spending has not (yet) picked up, the fact that business spending appears to be improving is a step in the right direction, analysts comment.

According to a number of market observers, the market is now more or less 'shut down' for the year, with a continuation of range-bound trading likely, given that large players with notable gains are not willing to put their winnings at risk. Others still believe however that we will see a continuation of the Santa Claus rally, suggesting that the strongest two weeks of the year are still to come (starting December 21) and that stocks will thus see more upside.

Next week will be abbreviated due to the Christmas holiday, yet the economic data calendar is loaded with plenty of economic data to be released on GDP, consumer confidence, home sales, import prices, demand for Durable manufactured Goods, and more. The key report is going to be Durable Goods on Thursday after the 2yr, 5 yr and 7 yr Note Announcement on wednesday.